For the past decade, US-based investors have exhibited a growing home bias, the tendency to overallocate to domestic equities relative to an optimized portfolio. This should come as no surprise, as domestic equities have outperformed foreign equities by more than 178% over this period[1]. This performance, coupled with persistent home bias, may introduce unintended portfolio risks that warrant careful consideration. In addition, attractive current valuations, favorable economic outlooks, and potential for non-dollar currency appreciation provide compelling reasons to reconsider your allocation to international equities in a strategic asset allocation framework.

International Equity: The Basics

Given the risks associated with concentrated domestic exposure, it is important to explore the broader global equity landscape, starting with the distinction between developed and emerging markets. Developed economies are characterized by high standards of living, robust economic growth, strong GDP output, and well-regulated, liquid markets. In contrast, emerging markets are still in the growth phase, typically exhibiting lower standards of living, smaller GDP output, and less mature capital markets.

Developed and emerging market economies are primarily tracked by three MSCI indexes: the MSCI EAFE (Europe, Australasia, and Far East) for developed markets, the MSCI EM for emerging markets, and the MSCI ACWI ex USA, which includes both developed and emerging markets—along with Canada—and effectively combines the EAFE and EM indexes.

Historically, the EAFE And EM indexes were narrowly focused within specific sectors; however, as global economies have evolved, these sectors have broadened. They now boast some of the world’s preeminent companies such as Novo Nordisk, TSMC, ASML, Samsung, Shell, and Tencent. While the AI trade has been focused on domestic firms like Nvidia, it cannot be ignored that the world’s largest chipmaker, TSMC, resides within the EM index and ASML, within EAFE, is at the forefront of chipmaking machines.

Diversification & Risk Reduction

International equities play a critical role in portfolio diversification by providing potential risk reduction and reduced correlations to U.S. markets, both of which could improve a portfolios’ risk-adjusted returns. In terms of risk reduction, international equities are significantly less concentrated than their U.S. based counterparts. For example, due to recent strength in domestic equities, this has led to a situation whereby the top 10 securities in the S&P 500 now comprise 37.9% of the index, amplifying exposure to a narrow segment of the market. Comparatively, the top ten securities in the EAFE index represent just 12.34%.[2]

Additionally, International equities broaden portfolio exposure to economies, sectors, and companies beyond the U.S. By expanding the investment universe, investors can reduce correlations across holdings, helping to smooth returns and lower overall volatility. It is important to note that during times of crisis, such as the Global Financial Crisis of 2008 and COVID, correlations tend to increase. There are other risks to consider when adding international equities to a portfolio. Investments are exposed to currency risks as well as global macroeconomic and geopolitical changes.

Despite these risks, the diversification benefit is particularly valuable given the current concentration of U.S. equities in many portfolios. For instance, when utilizing forward-looking assumptions[3], adding developed and emerging market equities to a traditional 60/40 U.S.-only portfolio the risk/reward trade-off has improved by just over 4%. Risk/reward is defined by the Sharpe ratio.[4] While incremental on its own, when paired with additional asset classes and other benefits of international investing, the result is a more resilient portfolio.

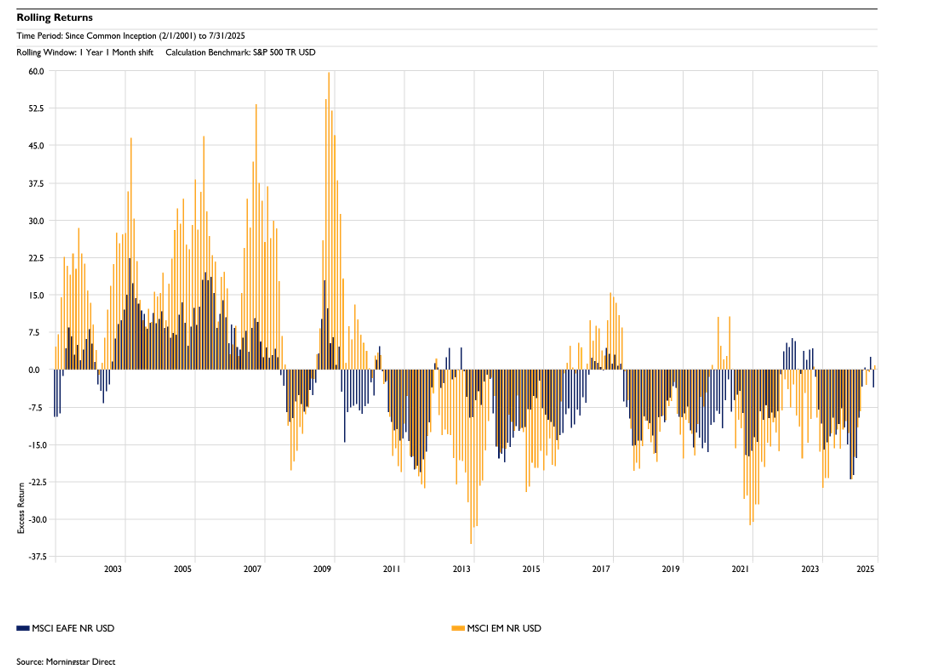

As shown above, relative to the S&P 500, international equity has underperformed over the last decade or so. However, there have been extended periods of international outperformance. These cycles go on throughout the history of the indexes, these cycles tend to last several years.

Valuation Opportunities & Mean Reversion

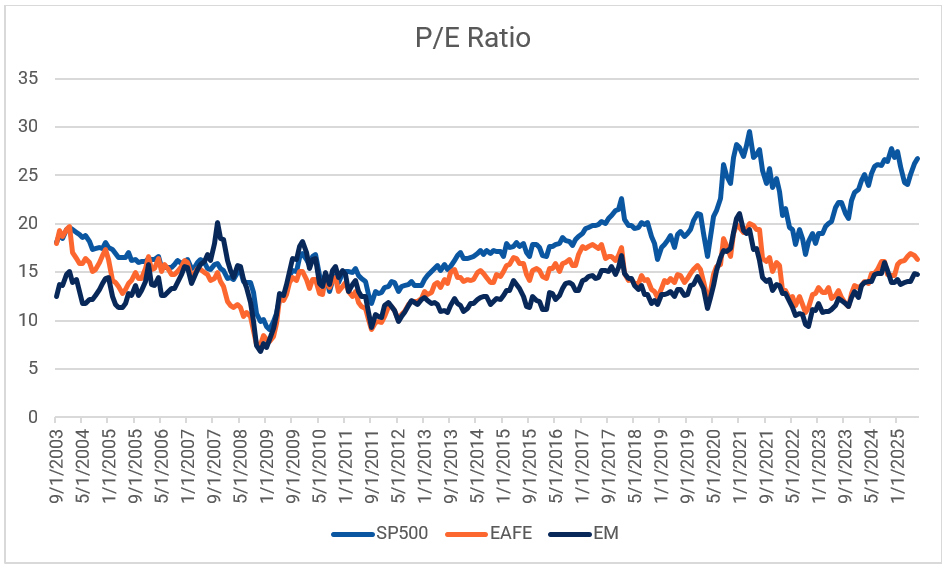

Relative valuations currently favor international equities. U.S. equities, as measured by the S&P 500, trade at a price-to-earnings multiple of 26.77, nearly two standard deviations above their 30-year average of 19.22. This is due, in part, to the high allocation to growth sectors within the S&P 500; the technology sector is 34.73% of the index. By contrast, international markets remain closer to long-term norms, offering more attractive entry points. MSCI EAFE equities trade at 16.34 versus a 30-year average of 14.76, while MSCI Emerging Markets equities trade at 14.42 versus an average of 13.38—both within one standard deviation of historical levels. These valuation gaps highlight the potential for mean reversion, positioning international markets for relative outperformance over time.

International Growth Exposure

Allocating to international equities allows investors to access growth opportunities beyond the U.S., including structural trends in emerging markets such as rising consumer demand, urbanization, and the expansion of the middle class. Developed markets also continue to provide leadership in sectors like industrials, technology, and healthcare, while region-specific reforms and policy shifts are creating additional tailwinds. In Japan, investor-friendly reforms aimed at more efficient capital use have boosted confidence and supported equity markets. In Europe, 2025 marks a turning point as nations increase defense spending to meet NATO commitments, and Germany lifts its long-standing “debt brake” to fund infrastructure and defense investment. These moves are viewed by many as being a decisive shift toward growth and modernization. Together, these developments highlight a more supportive environment for global investors and expand the opportunity set in international markets.

Currency Tailwinds in a Weakening Dollar Environment

International equities also offer potential benefits in a weakening dollar environment. When the dollar declines, the value of foreign earnings and assets increases in U.S. dollar terms, boosting returns for domestic investors. This currency tailwind provides an additional potential source of return at times when U.S. assets may be under pressure.

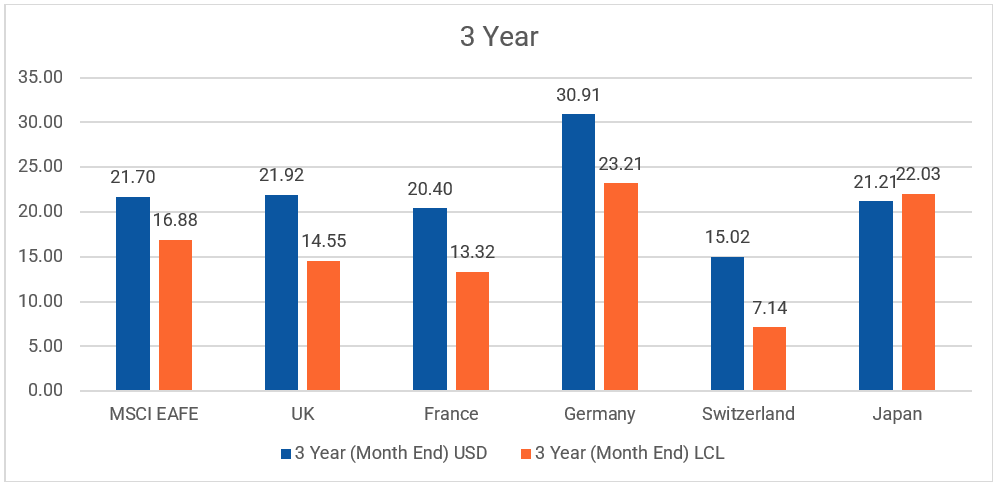

Illustrated in the chart below, since peaking at a 20-year high in the third quarter of 2022, the dollar has steadily weakened, and U.S.-based investors with international exposure have outperformed their local counterparts as stronger foreign currencies give US investors more dollars when exchanged. Meaning while European investors, investing in the Euro or Pound, earn a set return for their investments, American investors are earning more dollars due to the strength of foreign currencies.

Looking ahead, elevated U.S. fiscal deficits, narrowing interest rate differentials, and ongoing global policy shifts present potential for dollar softness, reinforcing the case for global diversification and international equities as a complement within diversified portfolios.

Conclusion: The Case for Global Allocation

Taken together, diversification benefits, attractive relative valuations, access to global growth drivers, and potential currency tailwinds make a compelling case for including international equities in a strategic asset allocation. While U.S. markets have dominated in recent years, history suggests that performance leadership rotates over time. Adding international equities can help diversify your portfolio and open the door to opportunities as global markets evolve. Connect with your Bolton consultant to explore whether this approach aligns with your objectives.